Key Takeaways

Instnt’s Identity Fraud Loss Insurance reframes fraud as a financial exposure that can be insured rather than an operating loss that must be absorbed. By transferring verified identity-related fraud losses off the balance sheet and into a predictable insured structure backed by A-rated carriers, institutions replace volatile write-offs with a defined premium and faster recovery, typically around 30 days. Combined with explainable AI decisioning, this model supports higher approval rates, steadier financial planning, improved capital efficiency, and reduced downstream operational burden compared to self-insurance or detection-only approaches.

Summary

- Treating fraud as an insurable risk introduces a more stable financial model for institutions navigating growth. Instead of relying on conservative reserves and ongoing adjustments to absorb fraud losses, verified losses are handled through insurance. This creates more predictable financial outcomes and reduces volatility from one period to the next.

- Instnt pioneered a new way to think about fraud by treating it as an insurable risk rather than an unavoidable operating loss. This approach introduces a different financial model for institutions that want to grow without tying up excess capital to manage uncertainty.

- Under this model, verified fraud losses are no longer absorbed directly on the balance sheet. Instead, they are transferred to A-rated insurance carriers through identity fraud loss insurance. The result? Less volatility in day-to-day financial planning.

1. Self-Insured Fraud Losses

Self-insuring fraud means the institution absorbs losses as they occur. While this approach is common, it places the full financial responsibility for fraud directly on the balance sheet and introduces challenges that grow more pronounced as volumes increase.

Under a self-insurance model, fraud losses are recorded as operating expenses. These losses reduce net income and create earnings volatility that can be difficult to smooth over time. With global fraud losses estimated in the trillions, the exposure does not end with a single write-off. The financial effects don’t stop at the initial loss. They tend to show up later in reporting cycles and planning discussions, often in ways that are harder to trace back to a single event.

After fraud occurs, teams are still involved well beyond the transaction itself. Activity has to be reviewed, documentation pulled together, and customers followed up with. That work runs alongside normal operations and adds cost gradually, rather than appearing all at once.

Check out how much fraud loss is costing you:

Because the financial impact is difficult to time or size precisely, many institutions respond by setting aside additional capital. Funds that could be used for lending or expansion remain parked as a precaution, which limits flexibility and affects how aggressively the business can plan from one period to the next.

On the operational side, self-insurance becomes something that has to be maintained. Fraud teams depend on a mix of systems, manual processes, and specialized knowledge that all require ongoing attention as patterns change. Controls are adjusted incrementally, review queues grow, and more legitimate activity is pulled into scrutiny. Over time, fraud management doesn’t level off — it becomes a standing function that continues to draw on both budget and people.

2. Instnt Identity fraud loss insurance

A new model has been introduced that treats fraud as an insurable risk rather than an unpredictable operating loss. Instead of forcing institutions to absorb fraud losses directly, verified fraud risk can be transferred to insurance, turning what was once volatile and difficult to forecast into a predictable expense. This represents a structural shift, not an incremental improvement. By separating fraud losses from day-to-day operating results, institutions gain greater control over financial planning and capital allocation. Fraud management becomes less reactive, operational decisions become more consistent, and growth no longer has to be constrained by uncertainty around loss exposure.

Loss Treatment

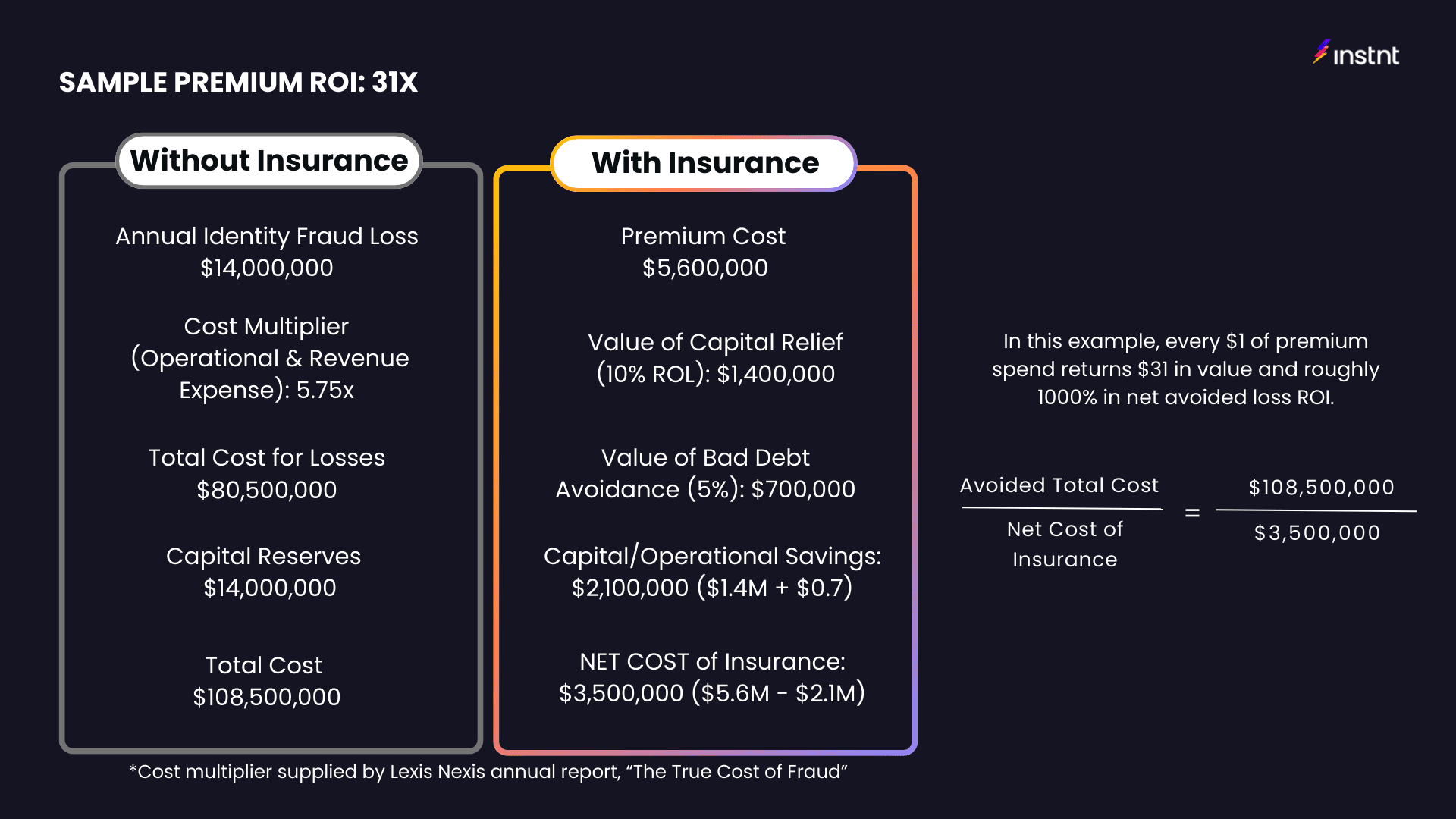

Under this model, fraud losses are transferred off the balance sheet to A-rated insurance carriers, including established global insurers. Rather than absorbing losses as they occur, institutions pay a consistent premium that represents only a portion of their expected exposure. When covered fraud does happen, claims are reimbursed on a defined timeline, typically within about 30 days. This shortens recovery cycles, prevents capital from being tied up for extended periods, and helps reduce volatility on the income statement.

Economic Impact

A fraud incident doesn’t close cleanly. Once it’s identified, related work continues to surface across teams, from reviewing activity to coordinating with compliance and responding to customers. That effort typically stretches over days or weeks and blends into normal operations.

As these follow-on tasks accumulate, they add cost and variability to normal operations. Time and resources are pulled into investigations and reporting, which makes expenses less predictable and complicates routine planning cycles like budgeting and forecasting.

“With fraud loss insurance, the financial impact shifts to the insurance sector, opening an opportunity for growth and innovation by leveraging tier 1 capital reserves.” – Sunil Madhu, CEO, Instnt

This level of predictability allows institutions to optimize capital allocation decisions with greater confidence.

Capital Efficiency

When fraud risk is handled through insurance, institutions no longer need to hold the same level of capital purely as a precaution. Funds that were previously set aside to cover potential losses can be put back into active use, improving day-to-day liquidity and easing pressure on reserves.

This changes how teams approach growth. With less capital tied up defensively, decisions around approvals become less restrictive, and fewer legitimate customers are declined simply to manage risk exposure. Insurance absorbs the residual fraud impact, allowing institutions to grow revenue without introducing additional volatility into financial results.

Operational Characteristics

From an operational perspective, the model is built to work alongside existing systems rather than replace them. Decisioning logic is transparent and traceable, which makes it easier for teams to support audits, regulatory review, and underwriting discussions without introducing new complexity. Coverage extends across identity fraud and related onboarding risks, so when fraud does occur, institutions are not left managing investigations, recovery, and remediation on their own. The insurance layer absorbs much of that downstream effort, reducing the operational lift that typically follows a fraud event.

When fraud losses are self-insured, institutions carry the full financial impact themselves, which often leads to earnings volatility and inefficient use of capital. An insured approach changes that dynamic by replacing uncertainty with a more predictable financial outcome.

Self-insured fraud losses place a direct financial burden on institutions, cutting into profitability and driving up operating costs. The unpredictable nature of these losses creates instability across financial planning and capital management.

Instnt’s identity fraud loss insurance shifts this uncertainty to A-rated insurers, converting fraud losses into a manageable, predictable expense. By transferring financial risk off the balance sheet, institutions reduce volatility and improve capital flexibility.

Fraud losses continue to weigh on financial institutions in ways that extend beyond the immediate impact. To protect against uncertainty, capital is often held in reserve, which introduces balance-sheet pressure and limits how much can be put toward growth initiatives. Over time, this defensive posture affects liquidity and makes financial outcomes harder to manage consistently.

Self-insurance reinforces this dynamic. When losses are absorbed internally, earnings tend to fluctuate, planning becomes more conservative, and operational flexibility narrows. Rather than stabilizing results, institutions are left adjusting to financial swings that complicate both growth and day-to-day decision-making.

Instnt offers a new model. By shifting fraud losses from the balance sheet to a predictable insured expense, Instnt enables institutions to stabilize financial outcomes, improve capital efficiency, and grow with confidence.

“Finance and Risk Officers can now add Fraud Loss Insurance to their risk management programs to shift significant losses off their balance sheets and transform risk reserves into working capital, boosting margins and enabling steady growth.” – Sunil Madhu, Founder and CEO, Instnt

Instnt’s fraud-loss insurance goes beyond risk transfer. It is a strategic financial discipline that helps institutions protect margins, optimize capital, and support sustainable expansion.