Summary:

The Current Expected Credit Losses standard has fundamentally reshaped capital planning for financial institutions. By shifting from an incurred-loss model to a lifetime expected-credit-loss framework, CECL requires institutions to provision for expected credit losses at the time of asset origination. This change elevates fraud from an operational issue to a balance sheet consideration. Our Identity Fraud Loss Insurance offers a capital-efficient approach within this environment. Insuring verified fraud exposure changes how it is reflected financially. With insurance in place, fraud exposure is reflected as a planned expense. Capital results tend to be more consistent, which supports steadier planning.

Key Takeaways:

- CECL Impact: CECL requires lifetime fraud loss recognition, increasing capital reserves and reducing retained earnings.

- Fraud Insurance Advantage: Transferring fraud losses to A rated insurers lowers Loss Given Default (LGD), directly freeing tied-up capital.

- Regulatory Compliance: Insurance premiums are treated differently from expected credit loss allowances. As a result, institutions can structure fraud exposure without increasing Adjusted Allowances for Credit Losses or placing additional pressure on capital ratios.

- AI Integration: Forward-looking fraud forecasting supports more accurate loss modeling and clearer documentation. Transparent and explainable methodologies align with CECL validation and audit requirements.

- Operational Efficiency: Claims are processed within ~30 days, rather than the long-term drag of self-insurance reserves.

The Capital Planning Shift

Regulatory frameworks have reshaped how institutions manage fraud losses and allocate capital. The CECL methodology, introduced by the FASB in June 2016 through ASU No. 2016-13, represents a significant shift in accounting practices. Moving from an “incurred loss” model to an “expected loss” framework, CECL requires institutions to estimate credit losses over the entire life of an asset, starting from its origination.

This shift has a direct impact on capital management. When CECL is first implemented, institutions typically see an immediate impact to retained earnings because expected lifetime losses are recognized upfront. Regulators allowed a gradual transition to help absorb that adjustment, giving institutions time to phase the capital effect into their financial reporting over several reporting periods rather than all at once.

CECL and Its Core Principles

CECL sits within ASC Topic 326 and applies to FDIC insured institutions. It sets the standard for how expected credit losses are calculated and reflected in financial statements. After it was adopted, regulators updated their guidance to stay aligned with the revised accounting framework. In practice, the change means institutions now build expected lifetime loss assumptions into their allowances from the outset, rather than waiting for losses to materialize.

As Federal Reserve Governor Michelle W. Bowman highlighted:

“The Federal Reserve’s regulatory approach must be capable of addressing and adapting to new activities and new risks but also must be constantly directed towards furthering our statutory objectives”.

This forward-thinking perspective mandates that institutions account for predictable losses, including fraud-related losses tied to credit instruments, as part of their upfront provisioning. This approach directly influences the amount of capital that businesses must hold in reserve, integrating fraud losses into the broader framework of regulatory requirements.

Fraud Loss Insurance Under Regulatory Requirements

Fraud, recognized as a critical operational risk, must be incorporated into credit loss allowances under regulatory guidelines. The Adjusted Allowances for Credit Losses (AACL), which reflect these expected losses, directly influence regulatory capital ratios. As a result, any expected fraud losses captured in the AACL reduce retained earnings and affect the institution’s capital position.

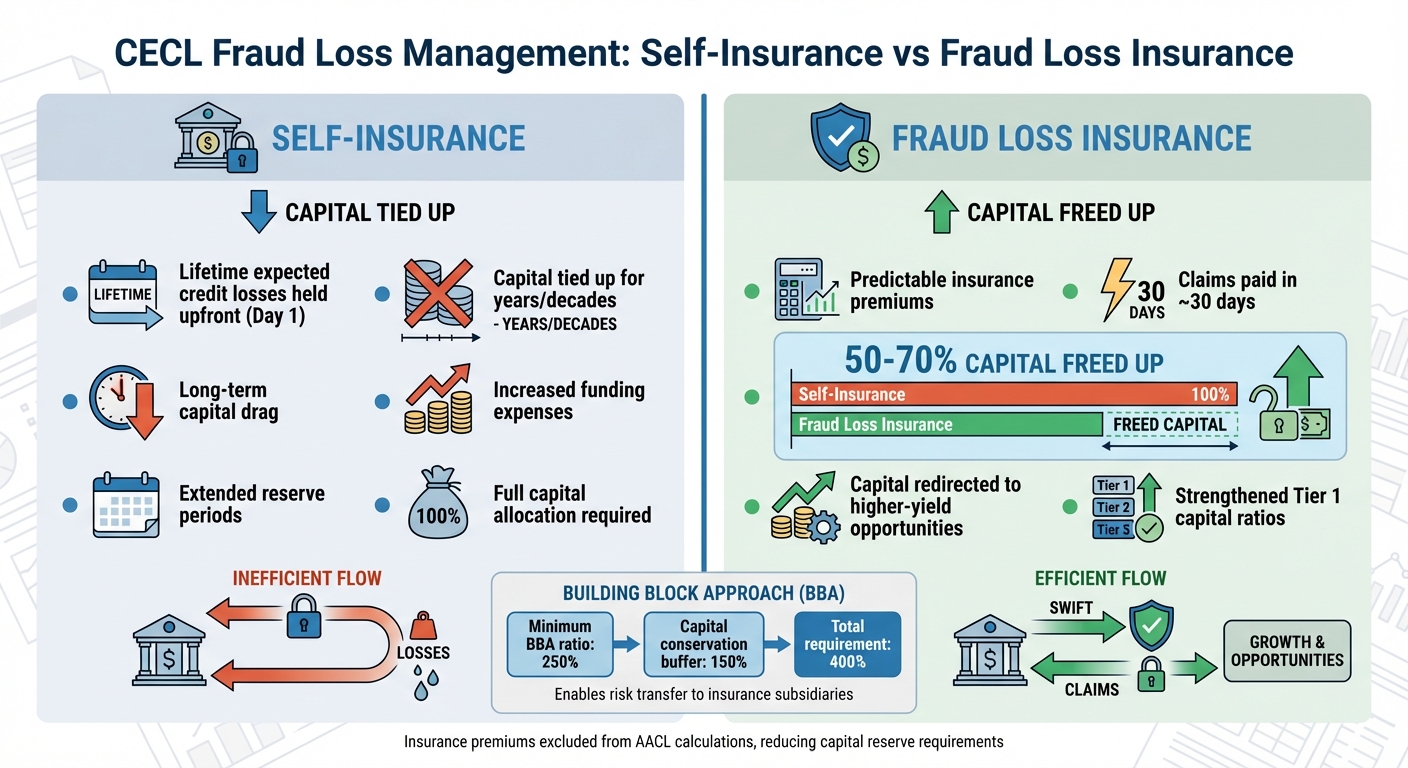

For financial institutions engaged in both banking and insurance activities, the Building Block Approach (BBA) aggregates capital requirements across these domains. Within this framework, a supervised insurance organization is expected to maintain substantial capital coverage under the Building Block Approach, including both a base requirement and an additional conservation buffer. Together, these thresholds are designed to ensure resilience across insurance exposures. When fraud risk is transferred through insurance rather than retained, institutions can adjust expected loss assumptions under CECL. That can help preserve retained earnings and support a more stable capital profile over time.

How CECL Affects Fraud Loss Insurance

CECL changed the way institutions factor fraud into capital planning. Instead of recognizing losses only once they are probable, institutions now incorporate expected fraud exposure into their estimates from the moment an asset is originated. That adjustment brings fraud assumptions forward in the reporting cycle and ties them more directly to reserve levels and capital calculations. This shift places greater financial and operational demands on institutions. As Tom Kimner, Head of Global Marketing and Operations for Risk Management at SAS, explains:

“The changes required by CECL require more detailed loss modeling, analysis, and reporting than what has previously been required” [7].

This evolving framework has significant implications for capital reserves and operational compliance, particularly in the context of fraud loss insurance.

Capital Reserve Requirements

Financial institutions must establish an allowance for lifetime credit losses as soon as an exposure is created. Fraud loss insurance plays a pivotal role in these calculations by influencing Loss Given Default (LGD). Under CECL, LGD is calculated as 1 minus the recovery rate. Since fraud loss insurance enhances recovery rates, it effectively reduces LGD, lowering required capital reserves and strengthening Tier 1 capital ratios.

Operational Changes for Compliance

CECL also changes how risk teams and finance teams work together. Because the standard relies on forward-looking assumptions, institutions must incorporate reasonable forecasts of future conditions into their loss models. When fraud exposure is covered by insurance, recovery assumptions need to be reflected clearly in those models. That means documenting how coverage works, how claims are processed, and how recoveries flow through financial reporting so the approach holds up under audit review.

Capital Allocation Strategies for Fraud Losses

Self-Insurance vs Fraud Loss Insurance: Capital Impact Comparison Under CECL

Self-Insurance vs. Fraud Loss Insurance

Self-insurance demands that institutions account for lifetime expected credit losses upfront—on Day 1. This approach ties up capital for the entire duration of the asset. In contrast, fraud loss insurance replaces long-term reserves with predictable insurance premiums. Claims are typically paid within about 30 days, allowing institutions to free up a significant portion of the capital previously tied up and redirect it into higher-yielding opportunities.

AI for Risk Forecasting

AI enhances the precision of fraud loss forecasting by analyzing extensive datasets and incorporating historical credit loss trends and macroeconomic data. AI strengthens the three core components of capital allocation: Probability of Default (PD), Loss Given Default (LGD), and Exposure at Default (EAD).

Transparency is a critical factor. Margarita Echevarria, arbitrator and mediator, highlights: “The transparency requirement acknowledges that the technology may outpace human understanding… the so-called ‘black box’.” Under CECL, institutions must quantitatively justify their forecasting decisions, making explainable AI (XAI) models indispensable.

Transferring Fraud Losses Off the Balance Sheet

Instnt’s approach addresses CECL-driven capital requirements by turning unpredictable fraud losses into fixed insurance premiums. One of the key benefits of this model is the ability to offset recoveries from operational loss events, which directly reduces the “Loss Component” factored into regulatory capital calculations. Additionally, claims processed in ~30 days help institutions maintain Risk-Based Capital (RBC) ratios above the critical 300% threshold.

AI-Managed Fraud Controls and Transparency

Instnt improves capital efficiency through AI-driven fraud controls. The system is self-learning and provides explainable AI models that meet the transparency standards required under CECL and SOX regulations. By detecting connections between seemingly unrelated entities, the AI uncovers sophisticated fraud schemes that traditional rule-based systems often overlook.

CECL Compliance Guidelines for Fraud Loss Insurance

Validation and Auditing

Regulatory guidelines mandate model validation every one to three years. Effective validation hinges on three components:

- Conceptual Soundness: Alignment with established accounting standards.

- Data integrity: Standardizing data across fraud tracking systems.

- Outcomes analysis (backtesting): Comparing predicted fraud losses against actual outcomes.

Explainable AI for Regulatory Trust

Explainable AI (XAI) allows institutions to trace how specific inputs lead to fraud predictions. Regulatory bodies classify AI used in insurance pricing or claims handling as “high-risk,” requiring detailed documentation. Instnt’s platform addresses these expectations with AI models that automatically generate audit trails, including timestamps and violation types, creating regulator-ready documentation.

The transition to lifetime expected loss recognition imposes immediate capital pressures on financial institutions. Strategic risk transfer—allowing fraud losses to be treated as insurable events—is a practical solution that excludes these losses from AACL calculations.

As regulatory landscapes continue to shift, financial institutions that incorporate fraud loss insurance into their strategies will benefit from strengthened capital ratios, clearer auditability, and enhanced operational flexibility that self-insurance reserves alone cannot deliver.